The teak critique

We analyse the sustainability of the desire for teak decking in view of the projected increase in demand from yachts in refit…

There’s a pressing need to accelerate our adaption of alternative decking sources, both for the well-documented environmental and humanitarian considerations and also to maintain the operation and aesthetics of the fleet. As well as a wake-up call, it also presents a significant commercial opportunity for the industry to invest in innovative solutions.

Teak decking – assessing market size

Much of the focus on the use of teak decking centres on its use in the new-build sector. However, a more significant driver of this will probably be from yachts replacing their decking during refits in upcoming cycles. The changing demographics of the fleet towards larger yachts and design conventions for large deck areas (and teak volume) have created a substantial market for decking.

While alternatives to Burmese old-growth teak do exist, the superyacht industry remains undeniably attached to its aesthetics and longevity. The distinct, unbroken golden hues of teak have become synonymous with classic yacht design, and the hardwearing nature of teak has been part of marine applications for hundreds of years.

However, this status quo cannot continue. The high demand for teak has led to deforestation and illegal logging in Myanmar, contributing to environmental degradation, human-rights violations and damage to the reputation of companies associated with this trade.

Part of the appeal of old-growth hardwoods such as teak is their longevity in marine applications. However, the majority of yachts will replace their teak sometime after between 10 and 20 years of cruising.

In 2021, the Council of the European Union imposed sanctions on Myanmar’s military regime, targeting its timber exports. The Environmental Investigation Agency (EIA) welcomed this move, highlighting the marine sector’s role in driving illegal teak-logging in Myanmar.

While not all logging operations are highly destructive, a significant portion originates from traditionally harvested regions that are essential to Myanmar’s economy. Nevertheless, the profits from this exploitation are inevitably linked to the military junta. Burmese old-growth teak is unsustainable, has limited supply and raises substantial ethical concerns.

In recent years, there have been positive developments in the industry.

In 2017, a consortium of leading superyacht builders and designers, including Feadship, Heesen Yachts and Oceanco, signed the Statement of Commitment to the Global Superyacht Industry Sustainability Charter, pledging to source sustainable teak.

However, the effectiveness of these self-policing initiatives remains to be seen because resistance to change is still prevalent in the industry. As with so many sustainability issues, a lack of data and reporting has hindered effective action. Without a baseline or forecast, it’s hard to quantify the issue.

Responses to requests by The Superyacht Agency for data from many high-profile and conspicuous consumers on the amount of teak they used were limited. However, there was positive engagement from some suppliers and installers of teak decking, and a list of teak-decking volumes used on a wide range of superyacht projects was compiled.

The analysis was fairly straightforward and took a few key considerations into consideration. Some yachts, if well maintained and relatively sedate with their operations, may never have their teak replaced. Part of the appeal of old-growth hardwoods such as teak is their longevity in marine applications. However, the majority of yachts will replace their teak sometime after between 10 and 20 years of cruising.

By collating the total amount of teak decking used across a diverse set of yacht projects, ranging from a 45-metre sailing yacht to a 127-metre motoryacht, a factor of cubic metres of teak per metre of LOA was calculated and then generalised into three sub-categories:

• 30-60m: 0.125 m3/LOA

• 60-90m: 0.29 m3/LOA

• 90m+: 0.48 m3/LOA

With the volumetric increase in size relative to LOA, the sharp increase in the amount of teak use is evident, with nearly four times as much per metre in the 90m category compared to the 30-60m sector.

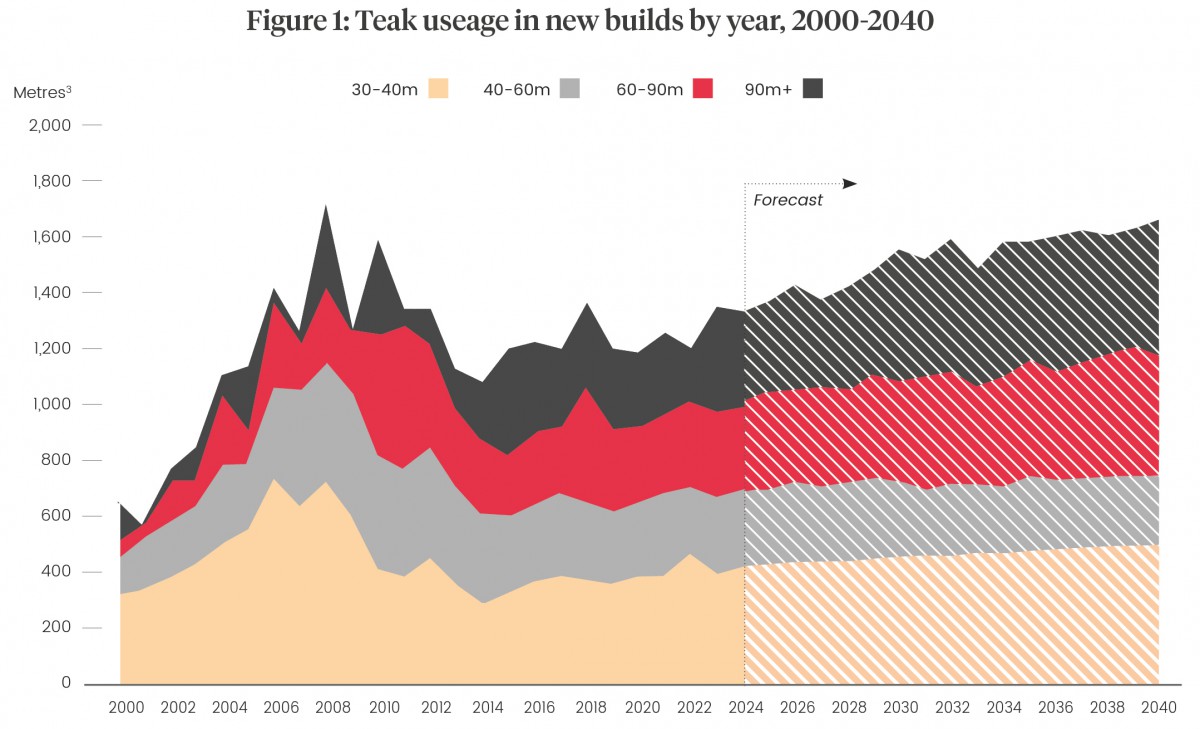

This data can then be overlaid with the 30m+ delivery numbers to give an estimation of the amount of decking in the fleet and its forecasted growth year on year. This analysis applied a conservative fleet growth factor to estimate the number of 30m+ yachts delivered by 2040 at roughly 160 units per year.

While there has been a limited uptake of non-teak solutions in recent years, as well as synthetic alternatives, the teak volume is roughly equal to the decking volume relative to the error margins of this analysis. For the purposes of this analysis, and based on the current fleet, ‘teak’ and ‘decking’ are used interchangeably.

Of the 108 90m+ yachts in the fleet, 84 have been delivered since 2000. These large yachts have a reciprocally higher teak volume per LOA, with the most teak-intensive motoryacht analysed being well over 0.50m3 of teak per metre

One of the key factors to highlight concerning the increase in decking volume is the expansion of the large-yacht fleet, especially the 90m+ sector since 2000. Of the 108 90m+ yachts in the fleet, 84 have been delivered since 2000. These large yachts have a reciprocally higher teak volume per LOA, with the most teak-intensive motoryacht analysed being well over 0.50m3 of teak per metre, and the average for this size sitting at 0.48m3.

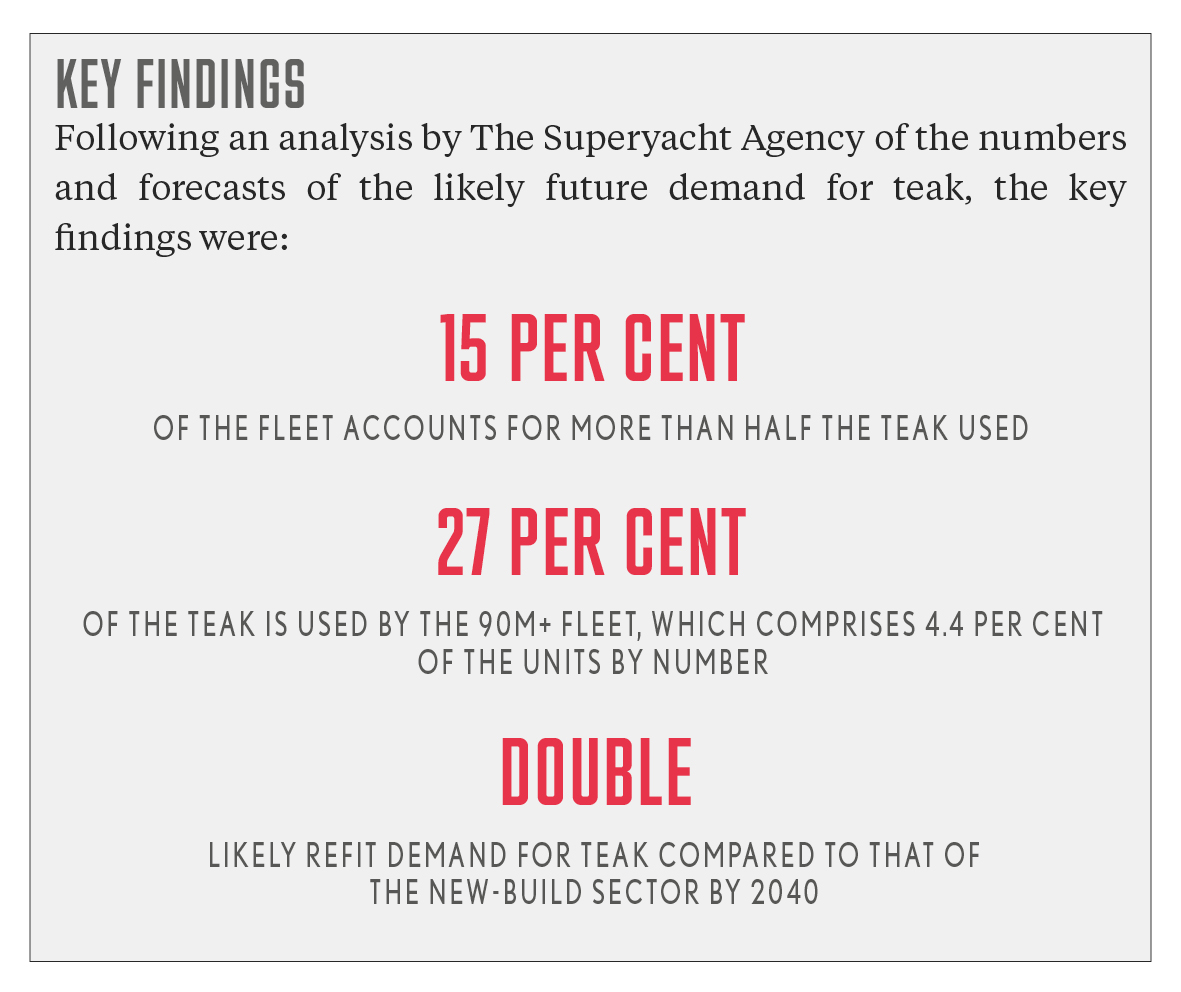

The impact this will have on the total demand from the new-build sector is outlined in Figure 1, with a conservative fleet growth estimate applied. Within these parameters, total 90m+ deliveries will level out at between six and nine per year by 2040. However, this sector still sees 4.4 per cent of the fleet accounting for 27 per cent of the teak. The number is similar for the 60-90m sector, which makes up 8.8 per cent of the fleet now, growing to 10.8 per cent by 2040 and accounting for 22.5 per cent of the teak.

These two sectors combine to make up 49.5 per cent teak usage for the fleet now, growing to 54.5 per cent by 2040.

This means that roughly 15 per cent of the fleet by units uses half the teak. This is a stark number now, but things get really interesting when we look further down the line. What happens when these big, multi-deck yachts with modern lines and long decks of unbroken teak start looking to replace them, especially when alternative uptake in the new-build space is still relatively small?

The refit model used was relatively simple, with two overarching assumed parameters:

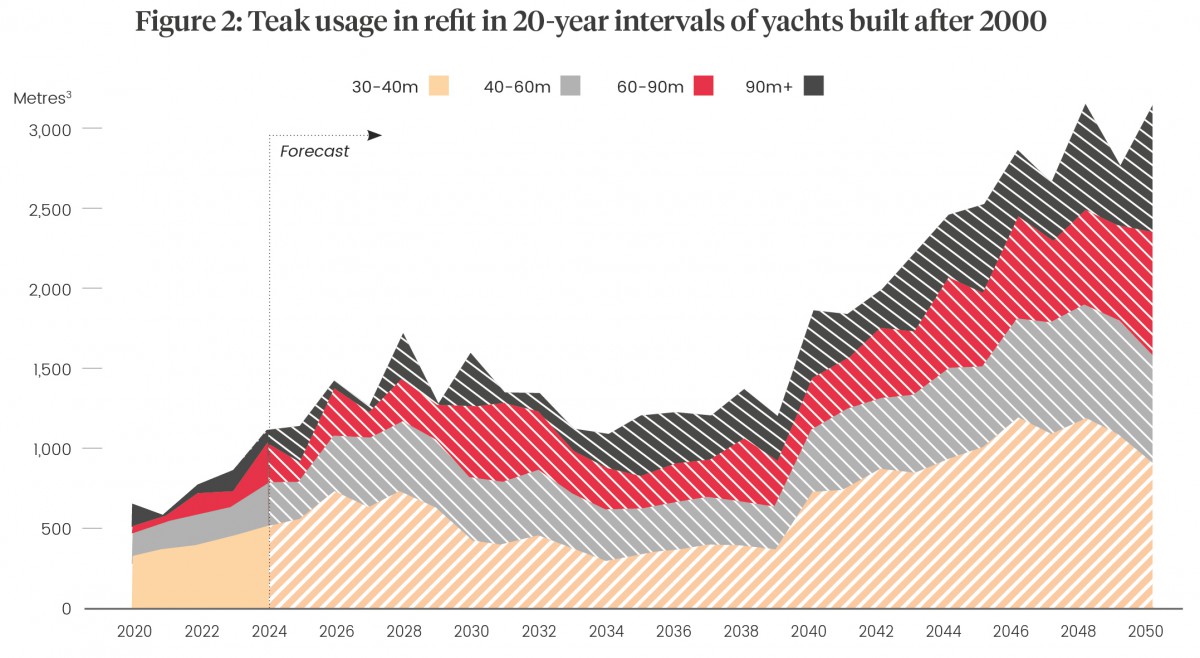

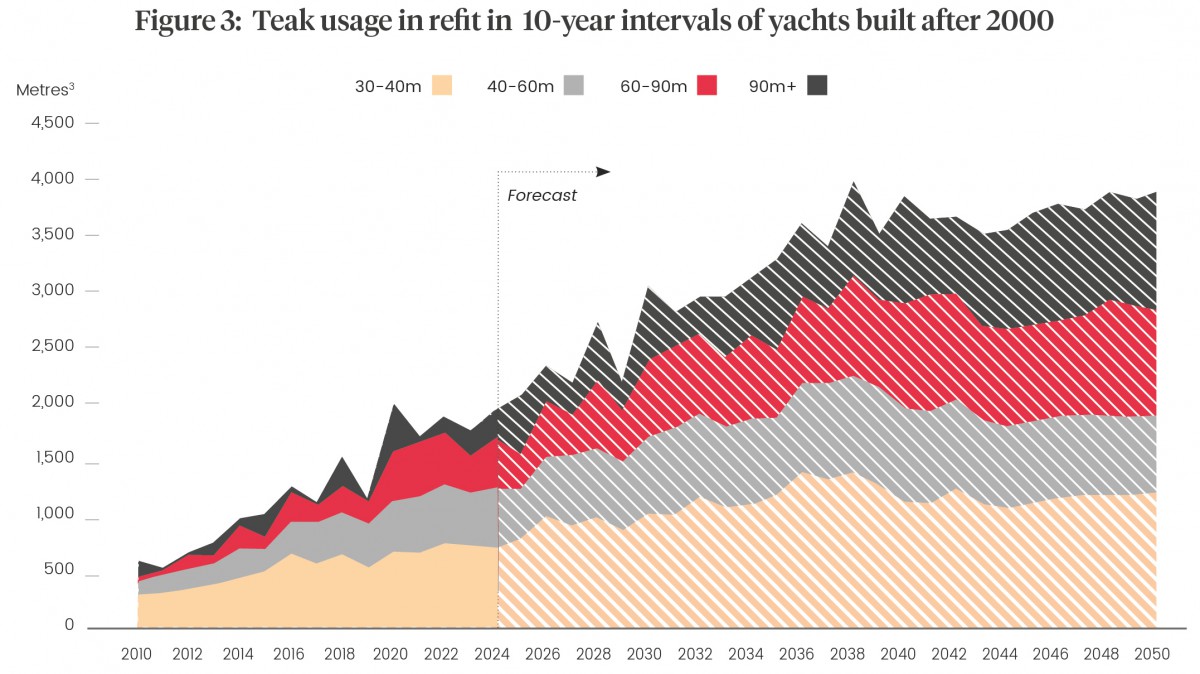

• Yachts built after 2000 will start to replace their decks after between 10 and 20 years of operation (both the 10- and 20-year intervals displayed in Figures 2 and 3).

• The new-build demand is assumed to continue at present levels, using the conservative fleet growth estimate outlined previously. Those yachts built since 2000 will also enter the teak-replacement model at the outlined 10- and 20-year intervals.

Demonstrating this in the data is the spike in demand in 2028 (Figure 2), which correlates to the reciprocal spike in deliveries in 2008 (Figure 1). Evidentially there is a high degree of variation between yachts and when they may choose to change their decking, but the inferred increase in demand is there, reaching a peak of around 3,000 cubic metres by 2048.

As the majority of these are larger and teak-intensive yachts, even based on the overly conservative 20-year teak-replacement cycle outlined, the demand for teak each year will more than double the assumed demand per year from the new-build sector today.

If these parameters are decreased to operate on a 10-year cycle, a conceivable timeframe for heavy-usage yachts with demanding owners, the trend is amplified significantly, with refit supply demand doubling the new-build demand by 2038.

Teak is known for its durability and, with proper maintenance, it can last for generations. Ensuring its sustainability hinges on effective management of the resources already in use. While some areas, such as the swim platform or sun deck, experience substantial wear and require replacement, many others, like protected walkways, may still have

several years of use left. The goal should be to recycle and reuse as much as possible but chemical processes in application make this difficult and many owners opt for a full-deck replacement.

The commercial pressure to supply vast quantities of old-growth teak persists, and it will require a collective effort from the industry to shift towards a more sustainable solution. As Richard Strauss from Teakdecking Systems aptly puts it, “The ultra-wealthy want what they want, but there is a finite supply.

“The commercial pressure for large quantities of old-growth teak still remains a significant challenge. Nevertheless, the industry has reached a pivotal moment regarding sustainability that necessitates a united effort. To shift the status quo to a more sustainable solution, we need to educate clients and the wider industry about the benefits of alternative materials. Embracing a more diverse selection of excellent alternative wood options that are readily available is crucial.”

Ultimately, if these materials are not readily available in Europe, yacht owners may opt to outfit their vessels up to the point of laying the deck and then transport them to regions with more relaxed import regulations. To safeguard these forests and their supply, this scenario must be prevented, emphasising the importance of educating the industry and clients about alternatives and presenting diverse, sustainable solutions.

According to a report from the Environmental Investigation Agency (EIA), as much as 40 per cent of teak imports from Myanmar, one of the largest wood exporters, finds its way into luxury-yacht construction. This demand has spurred illegal teak logging, particularly in Myanmar where corruption and lax law enforcement have allowed the trade to flourish.

What happens when these big, multi-deck yachts with modern lines and long decks of unbroken teak start looking to replace them, especially when alternative uptake in the new-build space is still relatively small?

Strauss highlights a positive trend in the increasing interest among yacht owners, representatives and shipyards in understanding teak supply chains and exploring alternative solutions. This shift in perspective, noticeable even at events such as METS, may signal a turning point for the industry as it steers towards a more sustainable future for teak.

Lürssen has shown its support for German-based Tesumo, whose modified wood process has been designed specifically for the yacht market. Developed as part of a research project conducted by Lürssen Shipyard and the German University of Göttingen, Tesumo uses natural, fast-growing wood, preferably from controlled sustainable forest management, as a basis and refined in a three-stage modification process.

Cork is another promising alternative. It’s known for its lightweight, inherent noise damping, low thermal conductivity and sustainability. Cork oak forests capture carbon dioxide and play a vital role in air quality. Cork oak is predominantly found in the Western Mediterranean region and North Africa, offering a sustainable source for this versatile material.

Other synthetic alternatives like Flexiteek are used in specific areas of superyachts, such as helicopter-landing areas and workspaces. However, the appeal of real wood underfoot remains unmatched, providing a sensory experience that synthetic materials can’t replicate.

In conclusion, as emphasised in the analysis, there’s the looming issue of a drastic increase in teak demand from the refit sector. Exacerbated by the increase in large yachts and their teak-intensive designs, significant pressure is likely to come on an already strained supply chain as this fleet looks to replace its decking in the coming years.

While industry players may deflect criticisms of the providence of the teak they use, the need to source a more diverse range of decking solutions and to be more efficient with current supplies is clear.

This article first appeared in The Superyacht Refit Report. To gain access to The Superyacht Group’s full suite of content, publications, events and services, click here to join The Superyacht Group Community and become one of our members.

Profile links

NEW: Sign up for SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek

Click here to become part of The Superyacht Group community, and join us in our mission to make this industry accessible to all, and prosperous for the long-term. We are offering access to the superyacht industry’s most comprehensive and longstanding archive of business-critical information, as well as a comprehensive, real-time superyacht fleet database, for just £10 per month, because we are One Industry with One Mission. Sign up here.

Related news

Class notations: a potential tool for progressing sustainability

Class societies have a role to play in advancing the sustainable design and operation of yachts, but are they maximising their efforts?

Crew

Corporate sustainability jargon busting

As more requirements come into effect that will directly affect the corporate world, we explain pertinent sustainability-focused terms

Technology

Out Now: The Superyacht Refit Report

Issue 219: The Superyacht Refit Report is now available to read and download online

Crew

Can the industry print a better future?

3D printing could be the antidote that shipyards are looking for to enhance sustainability credentials

Technology

Related news

Corporate sustainability jargon busting

2 years ago

Out Now: The Superyacht Refit Report

2 years ago

Can the industry print a better future?

2 years ago

NEW: Sign up for

SuperyachtNewsweek!

Get the latest weekly news, in-depth reports, intelligence, and strategic insights, delivered directly from The Superyacht Group's editors and market analysts.

Stay at the forefront of the superyacht industry with SuperyachtNewsweek